THE MARKET BIFURCATES AGAIN

SUMMARY AND CONCLUSIONS. The stock market has become bifurcated again. We would buy the "new leadership" interest-sensitive stocks, most drug stocks, and many big consumer growth stocks, into weakness; at the same time, we'd sell the "new downside leadership", big NASDAQ stocks, into strength, and we'd also reduce positions in the laggard energy sector on an anticipatory basis.

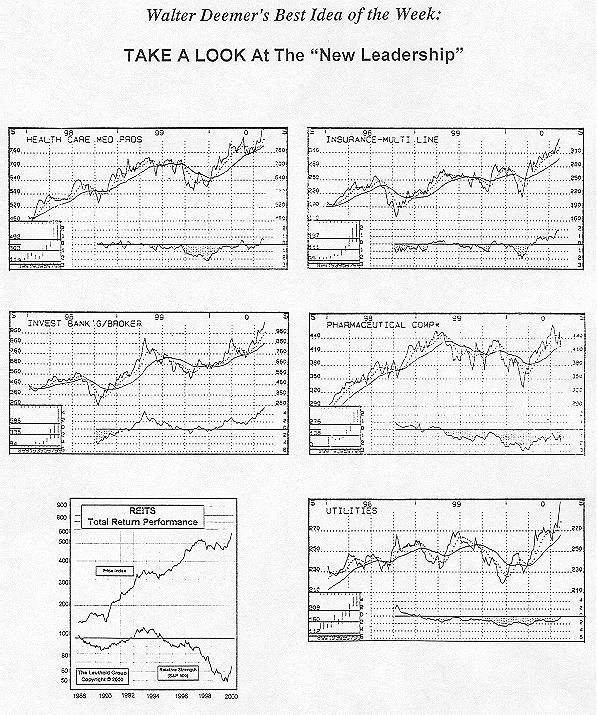

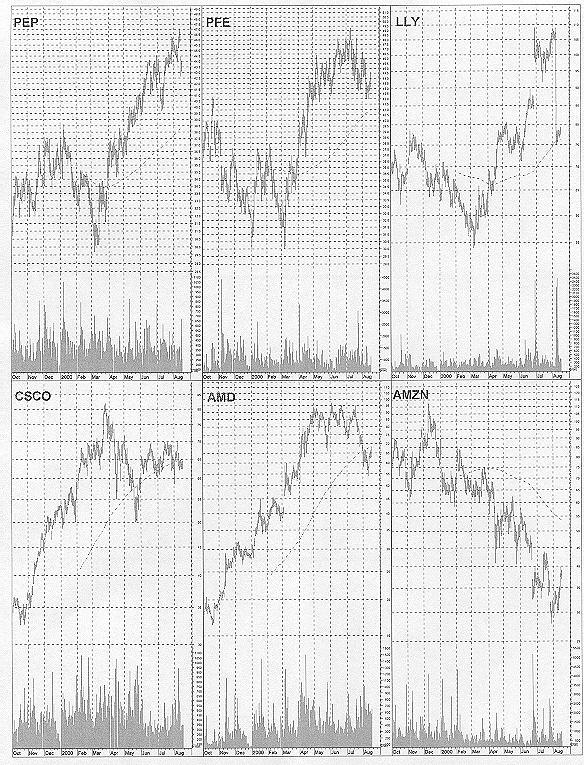

THE MARKET NOW. The stock market has become bifurcated again; this time, in a most interesting way. On the positive side, strength and upside leadership has emerged in the interest-sensitive areas of the market, particularly the utility and REIT groups and the financial sector; strength has also rotated into most drug stocks and many big consumer growth stocks. The strength in the traditionally-leading NYSE Financial index was diagnostic; during the past six weeks, the index has staged a persistent rally that ultimately carried it above its mid-1998 high -- and it generated relative strength all the way up. The key point in all this, though, is that every one of these groups is in the market's "leading edge"; from a long-term standpoint, then, it appears that the market's early movers have turned the corner and are heading back up again.

It certainly took them a while to do so, though. The NYSE Financial index, for example, topped out in mid-1998, and was some 25% lower than that when it finally bottomed in terms of relative strength in March -- which certainly qualifies as a full-fledged bear market in terms of both time and price. Similar declines were also seen in the other areas of "new leadership", as highlighted on the back page of the report. It thus seems reasonable to conclude that the market's leading edge entered a bear market in mid-1998 -- and that it ended that bear market this past spring.

The "new leadership", though, is not enough to support a full-fledged bull market, and it is therefore logical to assume that leadership will spread downstream at some point. The most obvious area for it to rotate into is the smaller stocks that have been so neglected for so many years; at the moment, though, neither small growth stocks nor small value stocks are showing signs of wanting to provide leadership for the market yet. We have been perplexed for some time as to why this should be the case, but DLJ's Tom Galvin probably has the most logical explanation: small stocks are under pressure here because they fear a credit crunch. Whatever the case, we expect upside leadership to spread SOMEWHERE at some point, and will continue to watch carefully to see when and where it does.

The interesting part of all this, though, is that while the market's leading edge was staging a bear market, the NASDAQ, which is a laggard area of the market, was staging an extraordinary bull run. It looks like that bull run ended this past spring -- and if the market's leading edge was an accurate predictor of the rest of the market, and if the leading edge entered a bear market in 1998 which continued for several quarters, the NASDAQ is likely to be in a bear market, particularly in terms of relative strength, for another year or more. (This also fits in with long-term historical precedents; when an area of the market makes an important speculative peak, history tells us that it takes a long, long time for it to correct those excesses.) The important thing, though, is that the NASDAQ is just as clear an area of downside leadership here as the market's leading edge is of upside leadership.

One other area deserves comment. The energy area is the most laggard area of all within the market. If the market's leading edge has just completed a multi-year bear market and turned back up again, and if the laggard NASDAQ has just made an important top, the currently-strong energy sector is likely to follow. We therefore believe that the current strength in energy stocks is much more likely to lead to a top of some importance than a significant further advance, and would thus use the current strength in energy stocks to reduce positions there.

As far as the "market" itself is concerned, what effect all these cross-currents have on the S&P 500 is anyone's guess. For what it's worth, we suspect the cross-currents will lead to generally lower levels for a while in the S&P; the market still has a host of longer-term negatives to cope with, and big NASDAQ stocks appear to have some unfinished business on the downside to complete. There is really more than one market out there, though, which we suspect will complicate our life (and these market comments) for some time to come.

THE BOTTOM LINE: We'd buy the "new leadership" interest-sensitive stocks, most drug stocks, and many big consumer growth stocks, into weakness. At the same time, we'd sell the "new downside leadership", big NASDAQ stocks, into strength; we'd also reduce positions in the laggard energy sector on an anticipatory basis.

STOCK COMMENTS. The "new leadership" is centered in interest-sensitive, drug and big consumer growth stocks (although it is more broadly-based in the first group than the other two). In general, though, we prefer stocks in those latter two groups; they probably have more upside potential as a group than interest-sensitive stocks do (particularly as far as the more defensive interest-sensitive stocks such as REITs and utilities are concerned). As far as WHICH drug stocks and big consumer growth stocks to buy are concerned, though, I'm afraid I must defer to fundamental analysis; the fact that a particular drug stock, or a particular big consumer growth stock, is not acting well does not NECESSARILY rule it out as a buy IF its fundamentals are strong. For what it's worth, though, PepsiCo and Pfizer look as good as anything in their respective groups, although we would confine buying those (and similar) stocks to periods of short-term weakness in them such as we are having now. Lilly of course, has had a lot more than a "normal" correction, but since it is an area of market leadership we'd be willing to buy it here.

On the negative side of the ledger, meanwhile, Cisco THE bellwether stock on the NASDAQ these days -- continues to trace out a secondary high in the 60-70 area. As we noted earlier, big NASDAQ stocks look like they have some unfinished business on the downside to complete, and we therefore regard periods of short-term strength in them as selling opportunities. The recent NASDAQ rally, meanwhile, was aided in no small way by a recovery in semiconductor stocks; chip stocks, though, are a laggard part of the NASDAQ, and they still look generally unattractive despite their recent strength. And, finally, most "investment-grade" Internet stocks remain in solid downtrends, and are thus continuing to provide downside leadership for the NASDAQ in general; we would therefore resist any temptation to do a lot of bottom fishing in that area of the market.

THE BOND MARKET is still stalled in the general area of its April high -- and bonds are doing a lot worse than interest-sensitive stocks, such as REITs and utilities, are doing these days. We think that bonds will outperform the stock market in general during the next couple of months, but it is unclear whether bonds will be able to generate absolute price gains while they are doing so. We would thus rather own interest-sensitive stocks than bonds here.

OUR OWN MONEY remains in a money market fund. A REIT or utility fund would probably be a better place for it at the moment, but we are not at all sure we are clever enough to hop out of a defensive fund back into a more aggressive fund when the time comes to do so. In addition, the next window of opportunity in the more aggressive area of the market should be in late September-October, and we do not like the idea of buying a defensive fund using that short of a time horizon. We are thus going to remain with our money market fund here.

BEST AND WORST GROUPS. Charts of the four best and worst-performing groups during the last seven weeks may be found, as usual, in the back of the report. To supplement those lists: Homebuilding rose onto the top four list for the first time this week while Aerospace/Defense fell off; meanwhile, Utilities-Telephone and Telecommunications-Long Distance fell onto the worst-performing list this week while Computer Software & Services and Consumer (Jewelry) resurrected. (The groups moving out of each category are probably the most timely to look at, since extreme strength or weakness is dissipating there; if you are able to anticipate such a move in one of the current top or bottom groups, though, it would be even more timely.)

OUR FIDELITY SECTOR FUND relative strength work was unchanged on balance this week as one fund, Business Services, rose above the money market rate of return but one other, retailing, fell back below it. This left the percentage of funds outperforming cash at 69%; the percentage thus continues to waffle back and forth between neutral and mildly-overbought territory without ever falling into fully-oversold territory, below 33%, which would set up a reversing "Buy signal". The holdings in our switching program, meanwhile, are unchanged from a week ago: the #1-ranked Brokerage/Investment Management fund (which was bought last week to replace the Electronics fund, which finally gave a "sell signal" after ten months), the #4 Energy Services fund and #5 Airlines.

MAJOR OVERSEAS MARKETS. The DAX continues to stage an orderly consolidation within a strong long-term uptrend, and is still the best-looking major global stock market. The FTSE, meanwhile, is going nowhere fast (it is at the same level that it was sixteen months ago), and still shows no signs of shrugging off its malaise. Finally, the Nikkei is continuing to march to the beat of a different drummer than other major stock markets; it still looks like it has a lot of long-term upside potential, but will have to demonstrate that it has found a sustainable shorter-term bottom before we get interested in it again.

-- Walter Deemer